The major indices on Wall Street have been on a relentless rally this year, as expectations that the Federal Reserve doesn’t have long to go in wrapping up its tightening campaign have bolstered appetite for risky assets. These are actively being traded as the US30, US100, and US500 CFDs on XM platforms.

A Mix of Optimism and Risk in the US Stock Market

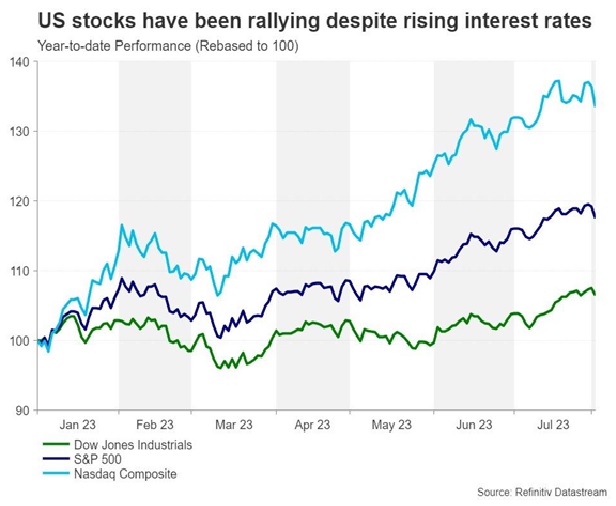

The S&P 500 has gained almost 20% this year and is a mere 5% from its all-time high, while the tech-dominated Nasdaq 100 has surged by more than 40%. Trailing behind is the Dow Jones Industrial Average, which has ‘only’ risen 7.5%. However, even traditional stocks that constitute the majority of companies listed in the Dow Jones have caught fire lately, as investors bet on a soft landing for the US economy.

Striking a Delicate Balance Between Inflation and Interest Rates

With inflation rates dropping sharply around the world, hopes are high that interest rates have peaked or are close to doing so. What is even more promising is that central banks have been able to get through this tightening cycle without causing a great deal of economic pain. But although there is good ground for optimism, are investors ignoring the risks ahead?

For one, it is probably premature to make the call that interest rates have peaked. Policymakers at the Fed, ECB, and others won’t be satisfied until inflation has fallen all the way to 2% in a sustainable manner. The Fed’s biggest fear is that inflation begins to creep up again once certain effects such as lower energy prices begin to wear off.

But even if persistently high inflation doesn’t force the Fed to overtighten, there is still a danger that the US could experience a severe credit crunch. The cocktail of quantitative tightening, tougher credit standards after the banking turmoil, and a deluge of new debt issuance by the Treasury Department are fast draining liquidity out of the financial system and this could eventually catch up with equity markets.

Potential for Downside Correction

When weighed against the already lofty valuations on Wall Street, the scope for a big downside correction is high in either scenario. Earnings are expected to have declined by around 7.0% in the second quarter, which would make it the worst quarter since Q2 2020 during the height of the pandemic. This makes it all the more questionable why the S&P 500’s forward price/earnings ratio of 19.7 (as of July 31) is currently running above its 10-year average of 17.4, according to FactSet.

But that’s not all. In the event that the US economy does avoid a full-blown recession, the assumption is that interest rates will begin to fall in line with inflation at some point in 2024. However, as long as the labor market remains very tight and there isn’t a new round of declines in commodity prices to prolong the disinflation process, the Fed won’t be in a position to cut rates as doing so would quickly fuel price pressures.

The longer Treasury yields stay elevated due to a hawkish Fed, the more challenging it will become for equities, particularly tech and growth stocks, to maintain their uptrend. This is because an increase in the yields of long-dated bonds also raises the discount rate used in valuation models for such stocks, negatively impacting the net present value of future cash flows.

Tech Stock Challenges and the AI Mania

The Nasdaq 100 is the most exposed to a repricing in Fed rate cut expectations and the Dow Jones the least. Though looking at the technical indicators, the Nasdaq has already started to lose some of its positive momentum, more so than the Dow Jones.

In support of the bulls, there is a new dynamic within the tech sector – the AI mania – that’s attracting fresh flows. With the so-called AI revolution only just beginning, valuations may not even come into the equation for some investors.

For more information, visit www.xm.com.